A decade after the late 2000s recession, much of the world is now back at the top of the economic cycle, and critically near the next crisis. At the top of an economic cycle, governments are collecting their peak tax revenues — yet, even so, many are still running large fiscal deficits and have large existing public debts. This includes the United States, Canada, and the UK among others.

With public finances in such a precarious situation, when the next recession hits, policymakers will be presented with dwindling options. Tax cuts and stimulus will be challenging, as the appetite for bond purchases by investors and central banks have already been stretched to their limits. This may be attempted, but especially with turbulence in global trade (affecting the supply of goods) and years of quantitative easing (affecting the supply of money), inflationary pressures would be too high to tolerate. In fact, one could argue that the consumer price index has already dramatically understated inflation with increases mostly accumulating in the real estate market, making housing unaffordable. Further monetary easing or fiscal stimulus would simply accrue more gains to the real estate market, due to land & tax policy which incentivize locations to be poorly used, monopolized, and prohibitively expensive. This is the Henry George Theorem, which demonstrates how government spending increases land values by more than this expenditure. Furthermore, the build quality, architecture, and locations of real estate projects have left much to be desired. Central banks are analogous to the driver of a car, but with so much of the lending injecting fuel into consumption and land speculation instead of more viable investment, it’s as if we’ve had our foot on the gas pedal for 10 years but the engine is broken.

Raising tax rates presents yet still more problems. Capital (and perhaps labour) will either make efforts to avoid these taxes, or will outright flee. There will be less to tax, and tax increases will slow the economy. Years of debt-fueled consumption buoyed by a soon-to-be deflating real estate sector have left consumers stretched far too thin for a consumption-led recovery. Yet lending in many countries has skipped over-investment in real production, which is where the monetary stimulus should have been flowing to all along. Poor tax policy has ensured that it did not.

What options will policymakers have to deal with the next crisis? With government and consumer spending out of fuel, and no room for tax increases to plug the deficit (without tanking the economy), the first place policymakers will look, will be back to the central banks. However, with central banks already stretched as well, they will have to become increasingly creative to achieve the same stimulative effect as before. This might mean outright and unsterilized monetization of debt. Some countries might still have room for such policies (which ones exactly will soon become clearer), however the majority will not be able to do so without severe inflationary consequences. Furthermore, if so little of the previous rounds of monetary easing resulted in productive investment, and instead led to unsustainable consumption, inflated asset prices, and property speculation, then more of the same rate cuts and quantitative easing will result in the same cycle once again. That is of course unless tax (and governance) reform addresses this.

The next place policymakers will look, will be to smaller government, and perhaps the unloading of obligations onto local governments. Improved governing efficiency and the streamlining of bureaucracy are absolutely necessary. However, the best time to take such actions is when the economy is running hot, so that the private sector can absorb laid-off public-sector workers. If there hasn’t been the political will to do so during times of growth, where will the political will be to take such measures during a recession? And if this is done during a recession, the expense of handling the unemployed will fall back again on government, especially with a population now drained of savings and mired in debt.

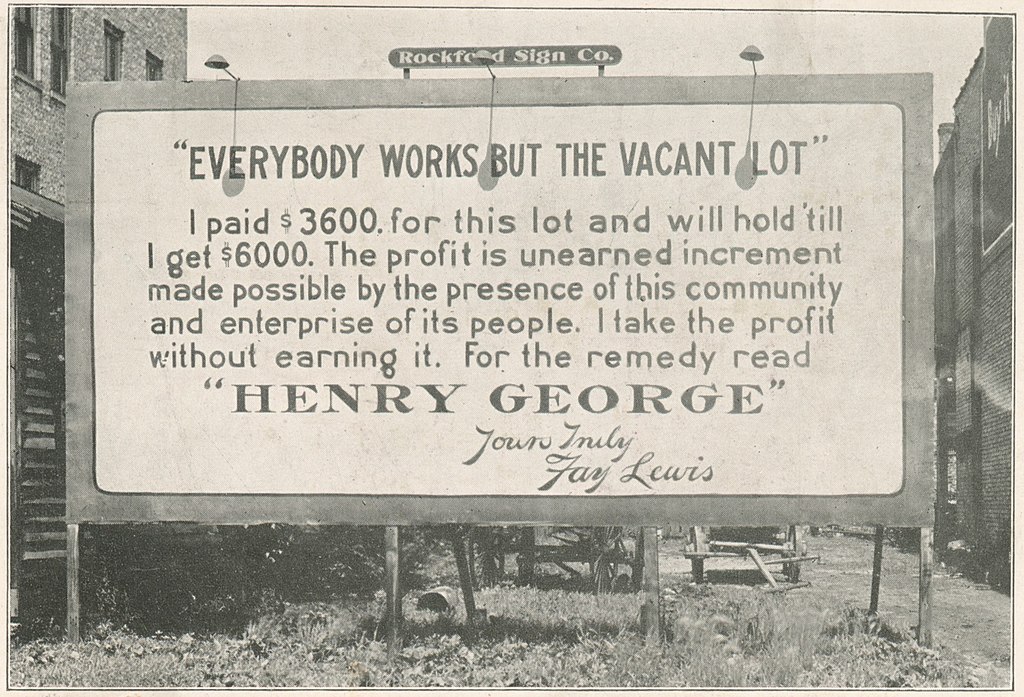

This leaves one final option: a shift in taxes on to unearned income, namely land value taxes (LVT). The LVT is not the same as a property tax, as it does not punish those who put the land to use; it taxes only the land, not the structure built on top of it. The benefits of LVT have been much discussed by famed economists across the political spectrum from Joseph Stiglitz to Milton Friedman. Unlike labour and capital, land cannot flee the country, or change in supply. It can be taxed without passing on price increases. It’s highly transparent, as property cannot be hidden, and it’s progressive — most of the rise in wealth inequality can be attributed to land. However, most of all, it is one of the rare taxes that does not diminish economic activity, and in fact stimulates it. It lights fire under the feet of land speculators and those underusing large lots of valuable urban land, putting it to its highest and best use. It pushes more units of housing onto the market, making them more accessible and affordable. It can also be combined with other incentives, proposed by the New Physiocratic League in the form of ULT, to shape our towns, cities, architecture, housing, commute times, and amenities in the ways we desire.

Going back to the Henry George theorem, since increases in government spending (particularly in infrastructure) disproportionately raises land values, a Land Value Tax makes infrastructure spending self-funding. Tax receipts would rise as a result of the investment. It would even allow for a reduction in transit fares, the gains of which would be recollected from the Land Value Tax

The Land Value Tax, particularly in the form of the New Physiocratic League’s ULT, could potentially be an urban planner’s dream. The ULT allows for regions to define desirable features in an area, including local architectural standards, environmental standards, and affordable housing, and apply the incentives to ensure their development. The Land Value Tax that underpins the policy pushes up growth from the earth, ensuring the most efficient utilization of space, and positive density – like clay rising up from a pottery wheel. Meanwhile, ULT incentives mould the clay into the forms that the population wants to see while maintaining architectural creativity. Strong economies, fiscal responsibility, and beautiful urban landscapes can, and must, thrive in harmony.