The prospect of buying a house seems so incredibly unlikely that many Millennials don’t even bother thinking about it. Having to pay an overpriced rent for potentially years to come is a fact with which most 20-somethings have come to terms, especially in London, the capital of staggering rents for less-than-perfect properties.

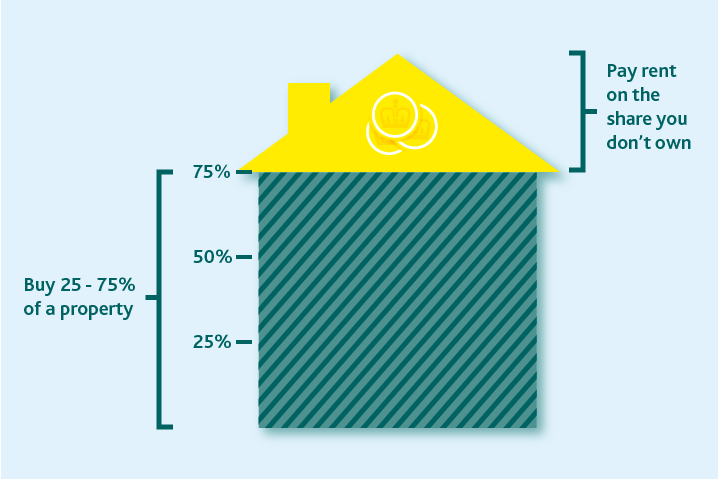

Still, there is a relatively little-known government-backed scheme that is aimed at turning the implausible phantom of owning your own house into a reality. Shared Ownership helps those who can’t afford to purchase a house outright, offering them the chance to buy a share of a property (between 25% and 75% of the full value).

If the thought of endless mortgage instalments gives you chills, fear not. You will only need to mortgage the shares you are buying, which makes a deposit significantly more affordable compared to the one you would pay when buying a property on the open market. Of course, you will still need to pay rent to a housing association on the remaining share, but you can decide to buy further shares of your house in the future.

Who is eligible?

Shared Ownership addresses mainly first-time buyers, though not everyone is eligible. You could start to get a foot on the property ladder through Shared Ownership if you are a first-time buyer and your household earns £80,000 a year or less outside London or £90,000 a year or less in London.

You are still eligible if you used to own a home but can no longer afford to buy one or if you are an existing shared owner looking to move.

Last but not least, you must be able to demonstrate that you have a good credit history and can maintain the regular payments and costs involved in buying a home. Easy peasy, right?

How does it work?

Once you have checked you are eligible, head to Share to Buy (sharetobuy.com), the portal listing all available properties in your areas or locations of choice.

When you have found ‘the one’, you will have to make sure you have the required deposit and get a mortgage on the shares you want to buy. If you’re not so good with the numbers, Share to Buy assists you with its budget calculator, which gives you an indication of the monthly costs you can expect to pay for the property you have selected.

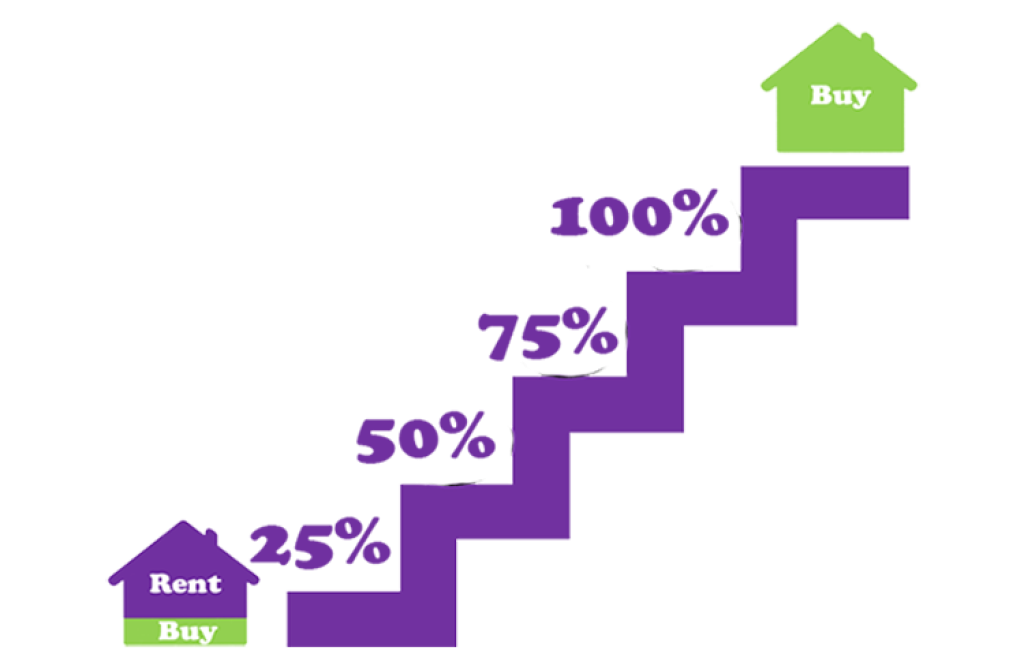

What is ‘staircasing’?

Staircasing allows you to purchase additional shares of the property you have bought through Shared Ownership. In most cases, you can staircase all the way to 100%, thereby owning the property outright. Thanks to staircasing, you can acquire further shares at a price equal to the relevant proportion of the current full open market value of the property. Share to Buy also provides a Staircasing Calculator which can help you work out if you have enough equity in your property to get a mortgage to buy more shares.

Pros and Cons

“First-time buyers have the advantage of 0% stamp duty on the first £300,000 of the purchase price on a property worth up to £500,000, which is a saving of up to £5,000,” says property expert Richard Blanco.

Stamp duty is a tax paid when buying a house over £125,000 in England, Northern Ireland and Wales. In its last budget, the government scrapped stamp duty for first-time buyers purchasing a home of up to £300,000.

Despite this decision, many first-time buyers using the Shared Ownership scheme may miss out on the exemption as stamp duty is calculated on the property’s full value, not the share purchased.

Staircasing can be tricky, too.

“If property prices are fairly stable over the next few years, that could make buying now and buying another tranche in two or three years a good strategy,” adds Blanco. “But if house prices go up, the extra chunks you buy in future will cost more and more.”

“If prices rise you only get a share of the uplift, making your next move as difficult as your first,” buying agent Henry Pryor echoes Blanco’s feelings.

“30-year mortgages on shared ownership is just another way of life telling you that you can’t afford it.”

So, while Shared Ownership helps first-time buyers put a foot on the property ladder, it’s well worth checking the rungs before climbing one’s way up.