Overseas investment in Britain’s property market is not a new phenomenon; empirically the opposite in fact. For centuries wealthy overseas buyers have been taking advantage of ineffectual property sanctions, investing in a secure market promising safe and assured returns. However, in the midst of an unequivocal housing crisis, in which society’s most vulnerable are unscrupulously paying the price, scrutiny is falling heavily on the shoulders of overseas investors. This article aims to examine how justified this criticism really is.

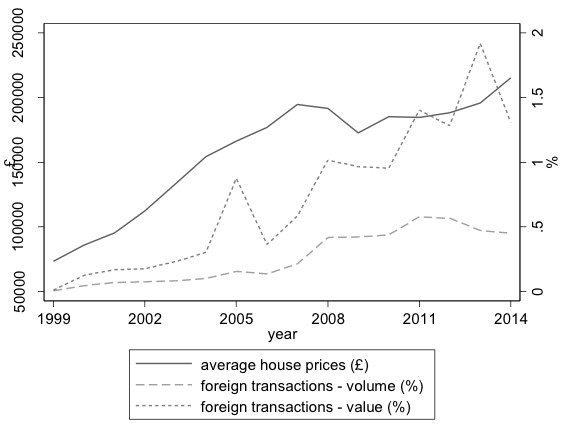

When it comes to foreign property investment; the meta-narrative is that overseas firms are pricing first-time buyers out of the market. Whilst there is a grain of truth in this assumption, it isn’t necessarily the case. Generally speaking, the properties acquired through overseas investment are predominantly ‘new-builds,’ costing primarily around the £1 million marks and above. Overseas buyers are undoubtedly in a completely polar market to your standard first-time buyer. It is no coincidence however that in recent years we have seen a steep upwards trajectory regarding the percentage of new-build sales concerning London’s total property sales. Savills estimates that in 2013 alone, overseas investors contributed £2.2 billion into London’s new-build sector, with over half of new-build property sales in Central London attributed to buyers from China, Russia, Singapore, Hong-Kong and Malaysia.

When it comes to new-build properties located in London a common trend has recently emerged; primarily that investors are now turning to the outskirts of the city to make their mark. If we look at the years 2014-2016, of the London based new-build properties priced at a minimum value of £200,000; only 6.6% were actually located in Prime London (Chelsea, Kensington Westminster etc). This is in contrast to 41.7% located in Outer London (Croydon, Sutton, Harrow etc.) The reason for this is simple; investors can get a lot more property for their money in these areas, with greater profits on offer. That said overseas investors have historically always been drawn to the Central London region; the City of Westminster has the highest proportion of overseas sales in London, with 11% of property sales performed involving an overseas investor.